2020 - Franco Angeli

Article PDF (0,26 Mb)

Pris en charge uniquement par Adobe Acrobat Reader (voir détails)

Are tax incentives determinant and relevant for capitalizing R&D expenditures? Evidence from Europe

63-97 p.

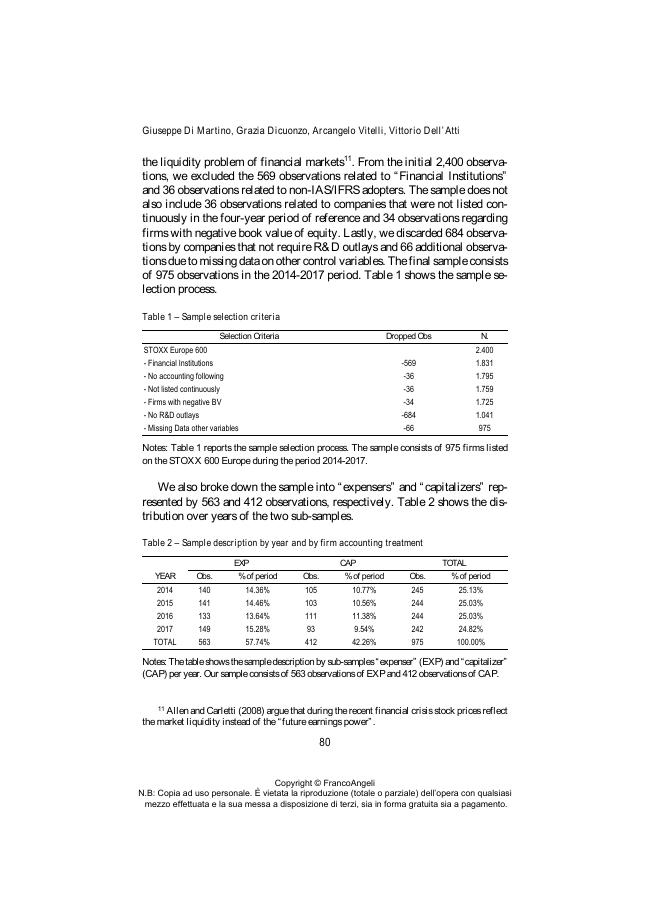

Using a sample of European listed companies between 2014 and 2017, we examine accounting factors that lead management to capitalize R&D costs, with a specific focus on the tax incentives in the form of government grants. In our analysis, we distinguish between companies which capitalize R&D costs ("capitalizers") and companies which expense R&D costs ("expensers"). The evidence shows that the choice to capitalize R&D costs is positively related to the recognition of grants as revenue. We also investigate the value relevance of tax incentives related to R&D expenditures. Our empirical findings show that investors draw a distinction between government grants associated with research costs (EXP) and those associated with development costs (CAP). This paper presents both theoretical and practical implications. It contributes to the current debate on expensing or capitalizing R&D costs through a study of tax incentives received by companies for their research activity.

Moreover, it offers empirical evidence on the use of R&D cost capitalization for purposes of tax incentives, which can be utilized by standard setters to assess opportunistic behaviors adopted by companies. [Publisher's text].

-

Articles du même numéro (disponibles individuellement)

-

Informations

Code DOI : 10.3280/FR2020-002003

ISSN: 2036-6779

KEYWORDS

- Accounting choices, government grants, R&D expenditures, tax incentives, value relevance